Markets in a Minute Beyond Our Borders: The Case for International Diversification

Key Takeaways

- International markets have outperformed the US to start the year.

- Economic theory and practice support the case for diversification, which remains a cornerstone of well-constructed portfolios.

- Valuations matter. US equity valuations are elevated compared to their long-term average and compared to the global opportunity set. While valuations are not predictive, expensive markets may be more susceptible to negative catalysts.

A Turning Point for Global Markets

After a stark shift in US tariff policy sent many US stocks plummeting, many investors started to look for a possible silver lining. In fact, according to Google Trends, there has even been a notable spike in the popularity of the phrase since April 2nd. One silver lining of market volatility in the US has been to highlight relative stability in other parts of the world, highlighting that global diversification remains a vital component of a well-balanced portfolio.

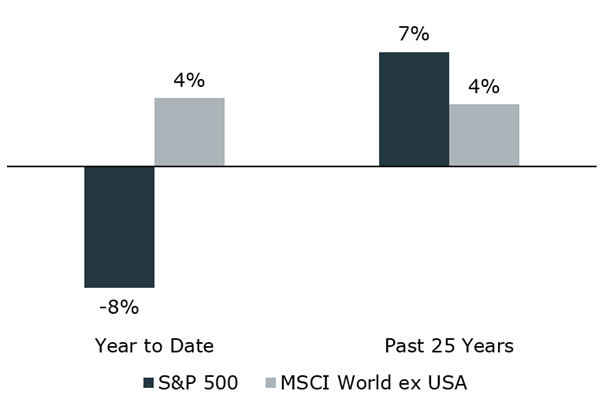

Year to date, international markets have outperformed the S&P 500. This recent outperformance is notable, because for much of the past 25 years international diversification has detracted from returns for US investors—and that relative performance has led many to argue that a US-only portfolio is sufficiently diversified (the fact that international diversification hasworked splendidly for the millions of non-US investors is a fact that is commonly overlooked, but is a point of view that we will address at another time).

Year-to-Date and 25-Year Performance of US and International Markets

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. For illustrative purposes only. Data as of April 14, 2025. “Past 25 Years” begins on April 1, 2000.

Highlighting a few months of international outperformance despite 25 years of underperformance is a classic case of searching for silver linings. But the case for international diversification does not rest on short-term performance—in fact, it does not rest on long-term performance either. In this piece, we will unpack some of the theory supporting the continued case for global diversification and highlight why the current global opportunity set remains an important part of today’s portfolios.

When Theory Meets Practice

Despite recent volatility and long-term skepticism, global diversification remains a critical component of well-constructed portfolios.

Diversification is a core tenet of modern portfolio theory, and a fundamental building block for investors. Global diversification helps reduce risk while providing exposure to markets with different sector compositions and growth opportunities than our home country.

Diversification isn’t just a theoretical concept—it reflects how markets function. For every buyer, there’s a seller. So, when an investor overweights their home market, they are inherently underweighting others. It’s unrealistic to assume all investors overweight their home country because they expect it to outperform. Yet many US investors have held that expectation for the US market.

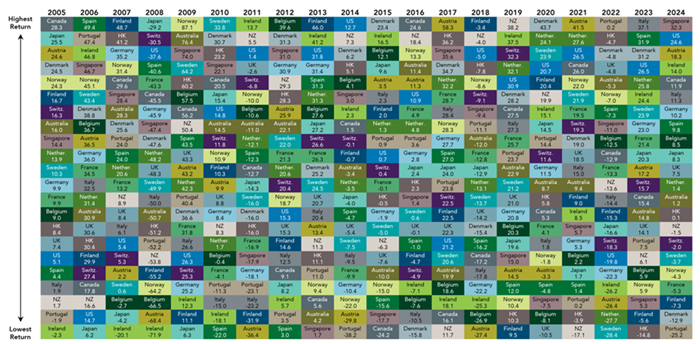

The US is the largest and most liquid market, supported by strong institutions and rule of law, and those factors may have contributed to the US exceptionalism that we have seen over the past decades. But a closer look reveals that while the US performance has been exceptional, it is rarely the best performing market across the globe.

Annual Equity Returns of Developed Markets

Source: Dimensional Fund Advisors. Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. In USD. MSCI country indices (net dividends) for each country listed.

The chart above shows annual returns across developed markets for two decades. What it does not reveal is much of a pattern. Recent history has many years of exceptional US returns, but the beginning of the sample has just as many examples of US underperformance. After a period of strong US returns, it can be tempting to forget about opportunities in non-US markets and disregard the risks of investing in US markets. As practitioners, it is our responsibility to balance both the risks and the rewards that markets across the globe offer. For those investors who are concerned about the US market, diversifying globally remains one of the most effective tools for mitigating risk.

Valuations Still Matter

Past performance does not give us reliable information about future returns, but how that performance materialized does contain insights. As we have previously discussed, much of the US outperformance over the past decade has been a result of valuation expansion—of US stocks getting more expensive relative to what those companies are expected to earn. While US valuations have come down from their levels at the start of the year, they are still well above their long-term average and above the levels of other markets.

Global Valuations

Current and 25-year next 12 months price-to-earnings ratio

Source: FactSet, MSCI, Standard & Poor’s, J.P. Morgan Asset Management. Past performance is not a reliable indicator of current and future results. Guide to the Markets – U.S. Data are as of March 31, 2025.

Valuations alone are not helpful to time changes in the market but high relative valuations in the US can make domestic stocks more vulnerable to bad news. And unfortunately, we did get some bad news. It remains to be seen if the US administration’s tariff policy is the beginning of a structural shift or just a blip for markets. But regardless of tariff policy, valuations will still matter. With high valuations and slowing growth, the case for continued US outperformance is harder to justify—making global diversification as compelling as it’s been in years.

The Takeaway

In recent years, it has been harder to defend international diversification as US stocks have soared. Yet for long-term investors, the theoretical and practical underpinnings of diversification remain evergreen.

Diversification is not about chasing past winners. The US has had an exceptional run of performance, but it remains unclear if that will be the case going forward. High valuations and slower earnings growth make the case less likely to materialize. The silver lining to all this is that investors have the tools necessary to mitigate uncertainty and build resilient portfolios. In an environment that seems likely to be dominated by uncertainty for the foreseeable future, the case for building a globally diversified portfolio is stronger than it has been for decades.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.