Markets in a Minute - China: Myths and Realities through the eyes of a dragon

The Chinese Loong, often translated as “dragon”, is a creature of legend: powerful, noble, and mysterious. Its head resembles a camel, its horns a deer’s, its body a snake’s, its claws an eagle’s, its scales a fish’s. Rarely does anyone glimpse the full Loong, as they live in the deep sea or the clouds. Most only ever “see” it in parts, and depending on which part they encounter, they walk away with vastly different impressions.

Modern China is no different. Some see a state on the edge of collapse. Others see a slowing country that’s losing its edge. Or, a rising superpower. They're all observing the same China, just from different angles, or through different lenses. Here we’ll unpack five myths about China’s economy and trade.

China’s Economy Is on the Verge of Collapse

Reality: China may look burdened, but the Chinese government has been willing and able to spend resources to support economic growth.

While the Chinese economy can no longer count on the double-digit growth it had once enjoyed, today’s mid single digit growth would still be the envy of many. In 2024, GDP expanded by 5%, and the IMF projects 4% real GDP growth in 2025, still stronger than most advanced economies (Source: IMF).

That said, the challenges are real. In the short term, China faces pressures from a deep property sector downturn, legacy local government debts, a weak labor market, especially youth unemployment, and persistently low or negative inflation. Over the long term, a shrinking workforce and aging population present structural risks.

To help address these headwinds, the government has deployed both fiscal and monetary tools. Fiscal measures include increased borrowing power by local governments, new funding for infrastructure projects, and lower taxes. To provide additional monetary stimulus, the People’s Bank of China (PBOC), China’s central bank, also cut the reserve requirement ratio (RRR) moderately, but preserved further policy room while waiting for economic data.

What to watch next: Two key factors will shape China’s near-term trajectory: external trade pressure and Chinese policy response. The potential for renewed or expanded U.S. tariffs could weigh on exports and sentiment. Attention is also turning to whether Beijing will introduce stronger fiscal stimulus or broader monetary easing.

China is Export-Dependent and Vulnerable to the U.S. Tariffs

Reality: Over the last several decades, China’s trade has branched in multiple directions - ASEAN (Association of Southeast Asian Nations), BRI (Belt and Road Initiative), and domestic markets, in addition to Western countries.

A common belief is that China’s economy depends heavily on exports, especially to the U.S. and other Western countries. While this was true in the early 2000s, exports now account for a much smaller percentage of China’s GDP at 20%, compared to 36% at its peak in 2006. (Source: World Bank). This shift is aligned with China’s recent efforts to prioritize domestic consumption and strengthen self-reliance.

China has also diversified its trade partners. In 2023, ASEAN countries became China’s largest trading bloc, surpassing both the U.S. and the EU (Source: China Customs). Trade with the U.S. now makes up over 11% of China’s total exports, down from 17% a decade ago.

U.S. tariffs, export bans, and Western reshoring efforts have influenced global supply chains. While U.S. tariffs provide a headwind to economic growth in China, they’ve reinforced Beijing’s push for self-reliance and closer ties with the Global South and Asian economies.

China is Losing Its Manufacturing Edge to Other Parts of the World

Reality: While some lower-cost production has shifted to countries like Vietnam, India, or Mexico, China’s manufacturing capacity has evolved, powered by its industrial clusters, technical talent and advanced production capabilities. It remains the world’s largest manufacturer, accounting for 27% of global manufacturing output, more than the U.S., Germany, and Japan combined (Source: World Bank).

China’s manufacturing strength mainly lies in these core areas:

- Cluster Effect: China has over 2,000 industrial clusters, from electronics to automotives, creating hyper-efficient ecosystems of factories and skilled workers. From Shenzhen’s high-tech hardware corridor to Cixi, a hardly-known county-level city that produces 60% of the world’s small home appliances, these clusters reduce costs, speed up R&D, and attract specialized labor.

- Technical know-how: Between 2000 and 2020, the number of engineers in China soared from 5.2 million to 17.7 million. Nearly 44% of these engineers are under age 30, compared to just 20% in the U.S., giving China a younger, more cost-effective base for innovation and industrial design (source: Bloomberg).

- Advanced production: China is the world’s largest user and installer of industrial robots, responsible for over 50% of global new installations annually. This powers a shift toward smart factories and automation (Source: WIPO). Recent WSJ coverage highlights the Chinese “dark factories”, where robots handle manufacturing with minimal human input, so the factories could run pitch dark.

Share of Total Operational Robots Installed (2006-2022)

China may no longer be the cheapest place to manufacture, but its production capacity is difficult to replace. The world still makes things in China not just because it can, but because it’s difficult to match the same scale, speed, and complexity.

China Makes, the West Invents

Reality: China has evolved from “brute-force imitation” to designing and patenting new technologies in areas such as artificial intelligence, advanced robotics and electric vehicles.

During China’s early industrial phase, its growth depended heavily on imported technologies and Western know-how, often being accused of stealing intellectual property. In contrast, more recently, China is outpacing peers in some innovation metrics, fueled by a talent engine that produces over 3.5 million STEM (Science, Technology, Engineering, and Math) graduates annually - more than four times the number in the U.S. (Source: CSET)

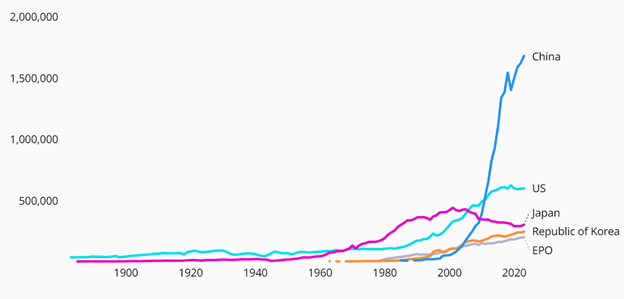

Patent activity reflects the innovation activities. In 2023, China filed 1.64 million patent applications, the highest in the world, and now holds over 5 million active patents, compared to 3.5 million in the U.S.. This indicates not just a surge in filings, but sustained, systematized innovation (Source: WIPO).

Trend in Patent Application for the top Five Offices (1883-2023)

Source: World Intellectual Property Indicators, 2024

Yuan Will Replace Dollar As World Reserve Currency

Reality: China’s renminbi (RMB), or Yuan, still lags significantly behind the adoption of the dollar in international trade.

Speculation that Yuan will soon rival the U.S. dollar has grown alongside talk of de-dollarization and expanding BRICS+ influence. Yet the global currency landscape tells a different story.

As of May 2025, the yuan accounted for 2.9% of global SWIFT payments, while the U.S. dollar dominated with 49%, followed by the euro at 23% (Source: Trade Treasury). In global reserves, the RMB held only 2.2%, compared to 58% for the dollar (Source: Bloomberg).

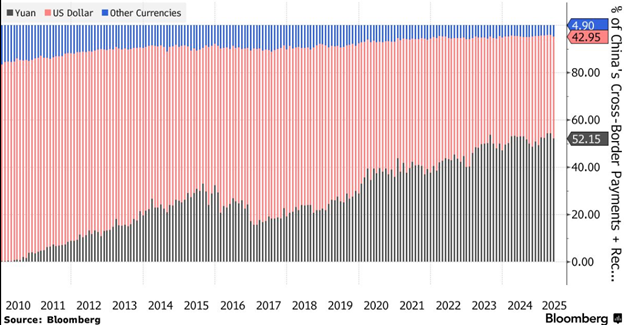

The Yuan has enjoyed some tailwinds. Over 50% of China’s cross-border settlements are in Yuan, and less than 5% of trades settle in the U.S. dollar. It has also expanded currency swap lines and piloted the digital yuan in international settlements. But capital controls, non-convertibility, and limited global trust in Chinese financial institutions remain significant barriers.

Yuan Takes Highest Share in China's Cross-Border Settlement

Conclusion: Seeing the Whole Loong

China’s economy is complex, evolving, and often misunderstood. Like the mythical Loong, whose camel head, deer horns, snake body, eagle claws, and fish scales defy simple classification. China looks different depending on which angle you view. Its growth is slowing, but not collapsing. Its trade is no longer West-dependent, but globally branched. Its manufacturing is shifting upward, not outward. Its innovation is increasingly homegrown, not copied. And its currency is moving, but still trailing global dominance. To understand China today is to see beyond isolated signals and headlines, to observe the full form of the Loong in motion: adaptive, durable, and still very much a force in the global economy.