Markets in a Minute – No Place Like Home: Pain Points in the Housing Market and the Path Ahead

If you’ve driven past half-finished subdivisions or watched apartment buildings rise in your neighborhood, you might assume that the housing market is on a roll. In reality, housing has been one of the weakest areas of the economy for some time — stuck in a rut characterized by a low supply of homes for sale and tepid demand tied to affordability challenges.

In this week’s edition of Markets in a Minute, we explore the state of the all-important housing market and its outlook. For this discussion, we focus on the single-family housing market, which makes up the largest share of the residential market.

Why Housing Matters

A home is more than a place to live. It’s where we make memories, form community connections and grow families.. For many individuals, their home is not only a place to live but also one of the largest assets on their balance sheet. According to Pew Research, home equity accounted for a median of 45% of homeowners’ net worth in 2021.

The housing market also has an outsized impact on the economy. It underpins a large swath of the financial services sector and drives spending on everything from big-ticket household items (like furniture and appliances) to construction material. Millions of Americans work in jobs tied, directly or indirectly, to the health of the market. In 2024, the market accounted for roughly 16% of product, as measured by spending on residential investment and housing services.

The Post-Pandemic Experience

Thanks to pent-up demand and low mortgage rates, the housing market came roaring out of the pandemic. But it began to cool in 2022 as borrowing costs surged, exacerbating long-standing affordability challenges that have priced many Americans, especially first-time buyers, out of the market.For many young adults, the homebuying process has become frustratingly long, if they succeed at all. The average age of first-time homebuyers reached an all-time high of 38 years old in 2024, according to the National Association of Realtors.

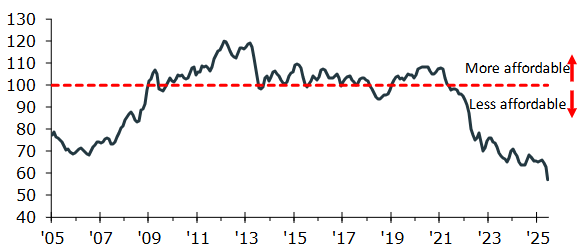

Home Ownership Affordability Index

Source: Kestra Investment Management with data from the Federal Reserve Bank of Atlanta. Data from January 2005 through April 2025

While many younger Americans are sitting on the sidelines, many older homeowners are feeling stuck in place — reluctant to sell and venture into a market defined by higher rates and home prices than in years past. According to a recent Redfin commission survey, more than a third of U.S. homeowners say they never plan to sell. The so-called lock-in effect among existing homeowners has suppressed both supply and demand.

In July, the national inventory of unsold existing homes on the market rose slightly from the prior month to 1.55 million, the equivalent of 4.6 months’ supply at the current monthly sales pace. After years of unusually slim inventory that pushed prices higher, months’ supply has now risen to its highest level in five years.

Where do we go from here?

While supply has shown signs of improving and mortgage rates have dipped lately, we may be a long way off from seeing a more-balanced housing market because of persistent structural issues.

Even if rates continue to fall in the near term, many would-be buyers may still find themselves priced out. Lower rates typically stimulate demand, which means already high home prices may rise further if the supply side of the equation doesn’t improve meaningfully.

Of course, lower rates are likely to entice many homeowners who have put off a move to sell, which would bring more shadow inventory into the market. The additional supply should alleviate some pricing pressure, but that may not be enough to compensate for the national housing deficit tied to years of underbuilding.

How did we get here? The global financial crisis, which had its origins in the housing market, has cast a long shadow. The crisis brought once-robust homebuilding activity to a near standstill, and it has yet to fully recover. Today, the U.S. is short an estimated 4 to 7 million homes

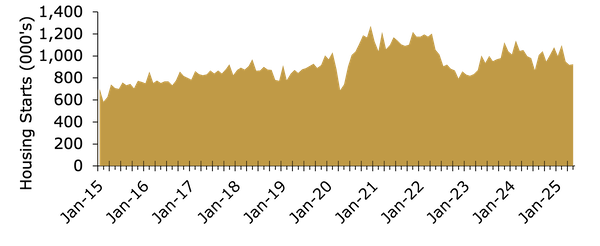

The outlook for the housing market depends a lot on whether homebuilders feel comfortable ramping up production. Right now, that doesn’t appear too likely. Since late 2021, homebuilder confidence has declined sharply and remained well below average. As a result, housing starts have fallen.

For many builders, it has become increasingly difficult to construct a home that the average American can afford. Elevated borrowing costs, high material and land prices, and labor shortages have driven up expenses. Higher tariffs are expected to put added pressure on input costs.

Housing Starts (Seasonally Adjusted)

Source: Kestra Investment Management with data from the US Census Bureau. Data from January 2015 – May 2025.

What can be done to ease the housing crunch?

Policymakers have been wrestling with the question for years, and they’re rolling out all sorts of proposals. The Trump administration, for instance, has proposed selling some federal land to increase the supply of land for building affordable housing, but the idea has met with opposition. Meanwhile, many cities and states have managed to scale back regulatory barriers, including zoning and environmental rules, that added cost and time to the homebuilding process.

Of course, the health of the housing market varies from place to place. As the adage goes, all real estate is local. In some metro areas, housing costs have climbed so far so fast that the markets have become especially vulnerable to downturns – much like high relative valuations can make stocks more susceptible to bad news. In other areas, affordability pressures are less extreme and the risks of downturn more muted.

We’ve seen some of these dynamics play out in our home base of Austin, Texas. After years of eye-popping growth, rents and home prices have been falling for months, although they remain above pre-pandemic levels. High housing costs have weighed on demand, while supply has increased partly as a result of zoning changes and other efforts by city leaders to increase density and affordability.

The Bottom Line

Given recent trends, the near-term outlook for housing is still murky, which means that the market’s contribution to economic growth will likely remain muted in the short term.

Yet there are some silver linings. The raft of policy proposals being floated across the country may alleviate some pressures. And while housing activity has stalled, household balance sheets remain strong. As a result, the market isn’t likely to be the catalyst for a broader economic downturn, as it was during the financial crisis.

Invest wisely and live richly,

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.