Markets in a Minute - Tariff Turmoil and Rebound: Second Quarter Market Review and Outlook

Key Takeaways

- The broad U.S. stock market saw another volatile quarter, starting with a sharp tariff-induced sell-off and ending at record highs. The S&P 500 index gained 6% year-to-date through the second quarter.

- The broad U.S. bond market extended its comeback. The Bloomberg U.S. Aggregate Bond Index returned 4% year to date through the quarter.

- Solid economic data, including cooler-than-expected inflation readings, helped push stocks to new highs. Yet many of the risks that triggered the second-quarter sell-off, including tariff uncertainty, are still a factor.

The start of summer often feels like a reset — a time to shed jackets, settle into longer days and look forward to family vacations. This year, the market gave us another reason to feel sunnier in the second quarter, staging a remarkable comeback after a rough start to the year.

In this week’s Markets in a Minute, we recap some key themes from the quarter, including pockets of outperformance and opportunity that should provide a tailwind for investors with broadly diversified portfolios.

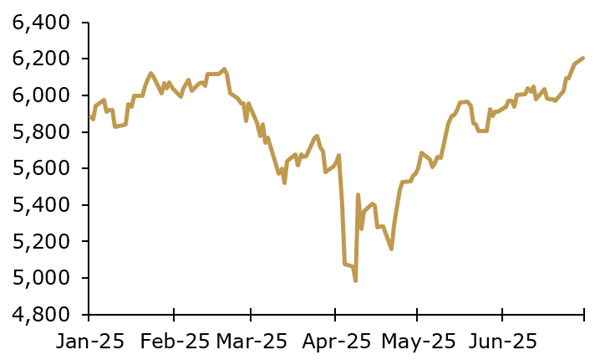

V-Shaped Recovery

The quarter kicked off with President Trump’s Liberation Day when the administration unveiled sweeping tariffs, sending stocks into a nosedive. However, the pain didn’t last long. Within days, Trump announced a 90-day pause on tariffs for all countries except China, and the market cheered.

On April 9, the S&P 500 gained more than 9%, among its largest one-day returns in history. By the end of the quarter, the index, which at one point was down by nearly 15%, had more than erased its losses.

Year-to-Date Performance, S&P 500

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Note: views are from a U.S. dollar perspective. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. Index data from January 1, 2025 through June 30, 2025.

Beyond the Bounce

As always, the market’s headline performance is only part of the story. Extending a rebound that began in the first quarter, international equities outshined their U.S. counterparts. International developed-market equities returned 19% year-to-date through the second quarter, more than triple the 6% gain for U.S. equities. That said, the magnitude of their outperformance has begun to narrow lately.

Value stocks — which had overtaken growth stocks earlier this year after a prolonged slump — lost some momentum as market leadership narrowed again. Still, we continue to see opportunity in value stocks, supported by attractive relative valuations.

Bonds Are Back

After years of disappointing returns, bonds have also been a bright spot this year, which is welcome news for investors seeking to diversify their portfolios. Within the Treasury market, we believe the so-called belly of the yield curve offers the most-attractive opportunity from a risk-reward standpoint. Yields on longer-term U.S. Treasuries are higher than (most of) their shorter-term counterparts, which generally suggests investors anticipate stronger economic growth and/or higher inflation ahead.

Treasury Yield Curve – December 31, 2024 vs June 30, 2025

Source: Kestra Investment Management with data from FactSet of the U.S. Treasury yield curve. Data as of June 30, 2025.

Over the past year, yields on intermediate-term Treasurys (5- to 10-year U.S. government bonds) have risen to levels not seen in years, offering investors a combination of elevated income and potential price appreciation if interest rates fall later in the year. (Bond prices tend to rise when rates decline and vice versa.)

Economic Resilience

Solid economic data underpinned the market’s rebound in the second quarter. Inflation has been milder than expected, and the labor market, despite signs of weakening, remains on solid footing. The unemployment rate (4.1% in June) is still enviable by historical standards, and job creation has been robust.

The generally positive economic backdrop has given the Federal Reserve room to take a wait-and-see approach to further rate cuts. The central bank is closely monitoring incoming data to assess how trade and immigration policy changes may impact growth, labor markets and inflation.

Risks Back in Focus

Stocks may have rallied, but some risks remain. Policy uncertainty continues to run high. The Trump administration set a July 9 deadline for lifting its tariff pause but subsequently pushed the date to Aug. 1. It continues to threaten to impose steep tariffs on many countries as it hammers out individual deals.

And although the passage of the administration’s “big, beautiful” bill eliminated some policy uncertainty, the legislation also raised concerns that higher spending and tax cuts could substantially widen the federal deficit and push up the national debt. These fiscal challenges are hardly new. They’ve been a uniquely American problem for decades now.

On top of fiscal challenges, we face more smoldering geopolitical risks than at any time in recent decades. The long-running Israel-Hamas war and conflict in Ukraine continue to grab headlines, and the second quarter saw U.S. military action in Iran, leading to a short-lived spike in oil prices.

The quarter also served as a reminder of the risks tied to market concentration and stretched valuations among the S&P 500’s largest stocks. A handful of mega-cap names drove both the sell-off and rebound, underscoring how dependent the broader market has become on their performance.

The Bottom Line

Perhaps the biggest takeaway from the turbulent first half of 2025 is that diversification is once again demonstrating its value. It can not only help protect portfolios from the kind of volatility we’ve seen in recent months, but may also position them to capture gains when overlooked areas of the market finally get their day in the sun.

Invest wisely and live richly,

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.