Markets in a Minute The Debate of Dollar Dominance: What Advisors Need to Know

Key Takeaways

- Despite recent weakness, the U.S. dollar retains significant structural advantages that support its global dominance.

- Shifting growth dynamics and policy signals have raised valid questions about the dollar's trajectory, but long-term implications remain uncertain.

- Currency hedging can reduce short-term volatility, particularly in fixed income, but has minimal impact on long-term investment returns.

For decades, the U.S. has enjoyed its role as the world’s reserve currency. This position lowers borrowing costs for the U.S., as global demand for dollars lets the government borrow at cheaper rates. Since markets benchmark other debt against U.S. Treasuries, businesses and individuals also borrow more affordably. For example, 30-year Treasuries help set mortgage rates, so homebuyers benefit from the dollar’s reserve status through lower interest costs.

But over the last few months, many have started to question how long the U.S. dollar can retain its preeminent status. There has been no shortage of discussion around the weakening U.S. dollar this year. This debate has happened before, but it previously occurred during periods of sustained dollar strength. Since the middle of 2015 through the end of 2024, the dollar gained nearly 14%. This year has been quite a different story, with the dollar dropping by nearly 9% year to date.

USD Index Level and Total Return—10 Years and Year to Date 2025

Source: Kestra Investment Management with data from FactSet. The USD Index as represented by the U.S. Dollar Index (DXY). Data as of May 28, 2025. Data begins on June 24, 2015.

Volatility in currencies is nothing new, but the speed and nature of the dollar’s turn downward has investors asking if this time is different—if this time, the dollar really is losing its status as a safe haven and reserve asset.

Is This Time Different?

The dollar has faced challenges before, but the structural advantages held by the dollar typically made investors shrug off the prospect of the dollar being dethroned. The structural advantages of the U.S. dollar include:

- The U.S. has the world’s largest capital markets, meaning companies can raise capital from investors easily and efficiently

- The U.S. has an openness to capital flows—foreign investors can easily invest in the U.S. and withdraw their investment

- The dollar is the main currency used to measure and settle international business—most global trade deals are priced and paid in U.S. dollars

- Many countries’ central banks use the dollar as a key guide when managing their own currencies (about 58% of global currency reserves are held in U.S. dollars)

- U.S. laws are clear and consistently enforced, which helps investors and businesses trust that their money and contracts are safe

Yet these structural advantages don’t make the mighty US dollar immune from challenges, the most recent of which is the sharp turn in trade policy. In April, the Trump administration shifted U.S. trade policy towards tariffs, prompting some investors and global policymakers to speculate that the dollar could be negatively impacted. With this shift in sentiment towards the dollar, it is worth examining how the dollar became mighty in the first place.

During the last 10 years, the U.S. economy grew on average by 2.5% while Europe and Japan grew by just 1.8% and 0.5% respectively. Higher growth in the U.S. helped drive demand for U.S. assets, including the dollar. In addition, higher interest rates and strong institutions in the US attracted capital inflows that reinforced the dollar’s strength. These factors helped drive the USD higher by 14% relative to a basket of currencies of our trading partners.

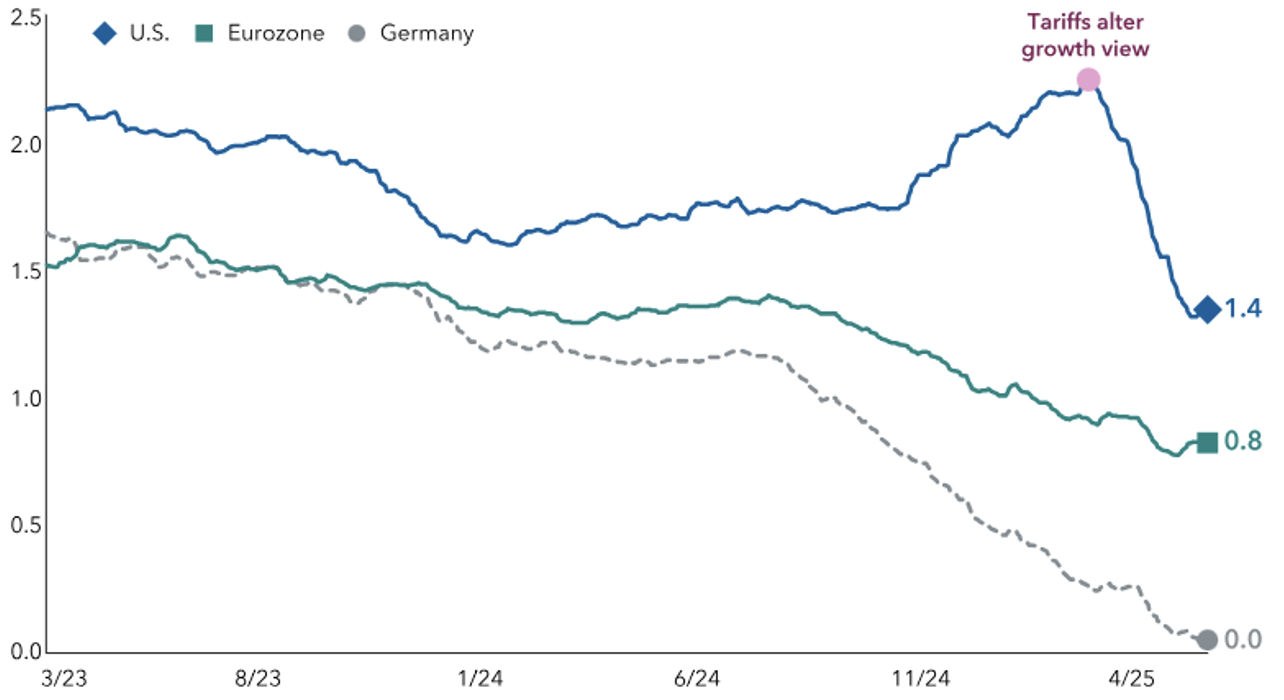

The higher tariffs recently introduced threaten to slow U.S. growth and contribute to a gradual dollar decline. According to Jens Søndergaard of Capital Group, the gap between U.S. and European growth appears to be narrowing (see chart)—and may explain some of the weakness earlier this year in the dollar. It is still unclear whether the shift is significant enough—or whether the changes in growth expectations will last long enough—to prompt the dollar to fall even further.

Global growth differentials are now less bullish on USD

Change in consensus GDP expectations (YOY%)

Sources: Capital Strategy Research, Macrobond. Data from March 1, 2023, to May 21, 2025.

A Dollar Under Pressure, but Not Dethroned

While recent dollar weakness has sparked renewed debate about the future of the U.S. dollar, history—and data—suggest that its foundational role in the global financial system remains largely intact. Structural advantages like deep capital markets, its dominant role in trade, and global reserve status continue to anchor the dollar’s prominence, even amid shifting economic and political landscapes.

That said, changing growth dynamics and evolving trade policies are legitimate reasons for investors to pay closer attention. Even the most dominant of currencies is not immune from challenges, as we saw during the gradual decline of the British pound over the 20th century. Whether the current environment marks the beginning of a lasting trend or just another cyclical downturn remains to be seen.

Given the uncertainty, some investors may try to hedge their dollar exposure, effectively removing the impact of a weaker dollar on their portfolio’s return. But simpler ways exist to manage this risk, like diversifying across non-U.S. stocks and bonds. Currency swings are sharp and hard to predict, and over time their impact tends to be close to zero. In global portfolios, currency fluctuations come and go. Long-term investors are generally better served by focusing on fundamental drivers of return—such as asset allocation, company earnings, and economic growth—rather than currency movement that are indistinguishable from noise over time.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Kestra Private Wealth Services, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.